Carried Interest: Essential Insights and Practical Tips for First-Time GPs

The past few years have seen a marked decline in fundraising, with GPs finding it tougher to raise new capital in light of the wider economic environment. One consequence of this we have seen is that managers are needing to be increasingly innovative with their fund terms to provide more flexibility to investors, with increasing numbers of side letters and complex waterfall models becoming more common.

Carried interest (often known simply as “carry”) represents the share of fund profits that the General Partner (‘GP’) will receive based on the value ultimately realised from the fund’s portfolio. Carry is in essence, a performance fee and is designed to ensure the GP has a meaningful commitment to the fund and is aligned with the interests of the Limited Partners.

The application of the carry concept is governed by the provisions of the Limited Partnership Agreement (‘LPA’), drafted by the fund’s legal counsel, and typically applies a waterfall model to define the order of priority in which profits are distributed between parties. The wording of the carry provision often provides for a degree of subjectivity, and this can present challenges for a GP when implementing in practice.

In this article we look at the practical considerations for first-time GPs when selecting the carried interest mechanics for their fund.

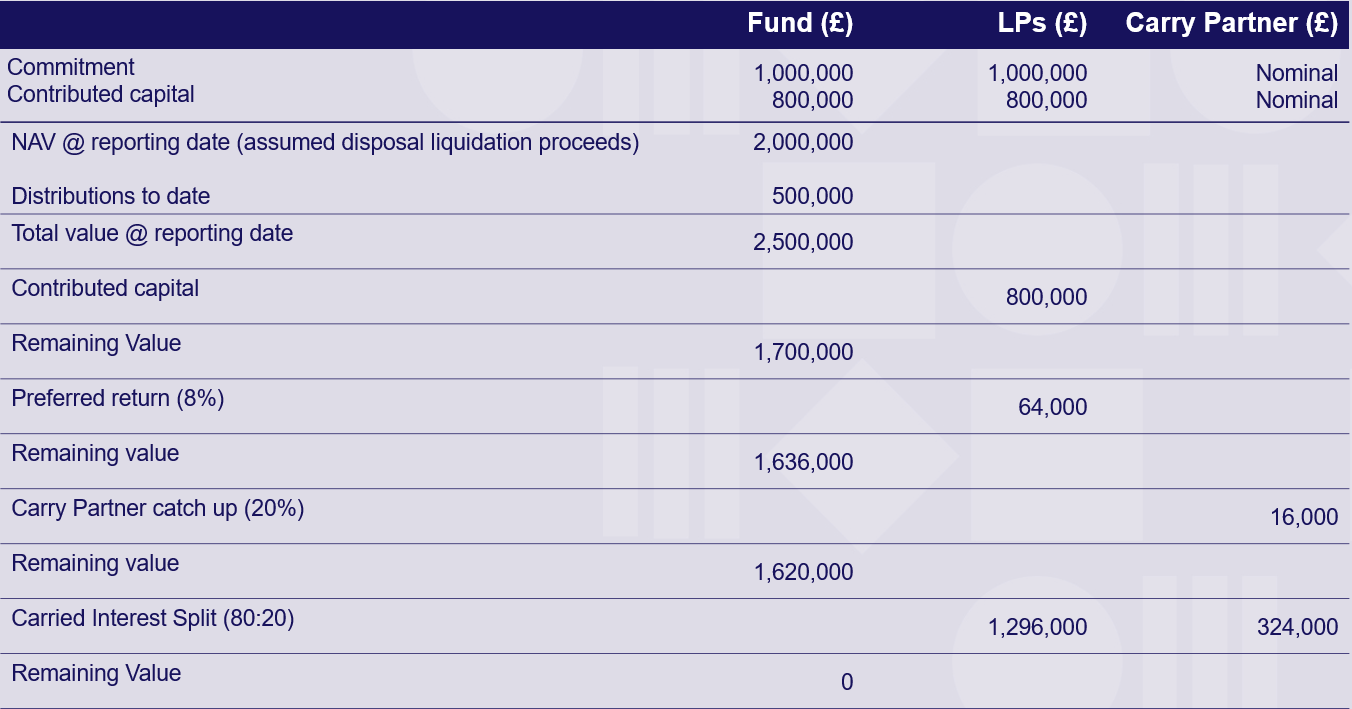

Understanding the waterfall model in Private Equity

The distribution model is often referred to as a “waterfall’ as it defines the order of priority in which distributions are allocated within the context of the overall profit-sharing (or ‘carry’) arrangement. The term waterfall can conjure up images of sizeable and overly complex spreadsheet calculations however understanding the overall objective makes these models much easier to digest and implement in practice.

In a typical waterfall model the GP will be entitled to a portion of fund profits (commonly 20%) but this will be allocated only after the Limited Partners have been returned any outstanding capital plus a ‘preferred’ return. The prioritisation of Limited Partner returns results in the need for a GP catch up before any remaining profits are distributed in line with the overall profit-sharing arrangement (e.g. 20:80 split).

European vs US Waterfall Model: Key Differences

There are two widely accepted applications of the waterfall model, the US (or deal-by-deal) model and the European (or whole fund) model. The concept is similar under both, however the European model considers cumulative contributions and realisation proceeds whilst the US model considers contributions and realisation proceeds specific to each deal. Under the US model there is no offset between “good” and “bad” deals and a mechanism is required to allocate fund level expenses and management fees to each individual deal; tracking investors pro-rata share of each deal is critical. The European model aims to provide the same overall distribution split by the time of the final distribution, however low-return deals towards the end of the fund’s life bring a greater risk of claw-back. It is important for GPs to consider industry standards and Limited Partner expectations when deciding on the preferred approach.

Role of Preferred return in Private Equity

The preferred return (or ‘hurdle’) is a component of the waterfall model which ensures that the Limited Partners receive their share of fund profits in priority to the GP. This offers some protection to the Limited Partners if profits aren’t sufficient to achieve the overall profit-sharing arrangement and ensures they are rewarded as a priority in return for risking their capital. The preferred return is calculated based on capital contributed and typically at a rate of 8% compounding annually from the effective date of contribution.

Practical considerations for carried interest

- Investor-Specific vs. Aggregate Waterfall Application – will the waterfall model be applied on an investor-by-investor basis or aggregated at a fund level? Investor specific side letters are becoming more common place amongst institutional investors and this in addition to excused investor and Family & Friends provisions can make the application of an aggregate model difficult to apply in practice.

- Preferred return – at what point should the preferred return stop accruing? In a European model it is typical for the preferred return to align with the timing of distributions i.e. as outstanding capital contributions are returned the preferred return on those contributions will cease to accrue. The preferred return will then continue to accrue on outstanding contributions until the point where distributions exceed outstanding capital as a whole.

- Subsequent fund closing – on what basis does the preferred return accrue for subsequent investors admitted after the initial close? In the spirit of being fair and equitable, GP’s will typically apply the same approach as capital equalisations; the preferred return is calculated from the date the subsequent investors drawdown would have been due had they been in the fund from the initial close. For the wider investor base the preferred return is typically applied to an investors equalised capital contribution.

- Recycling provisions – how are recycling provisions applied in the calculation of the preferred return? For example, if amounts available for distribution are retained by the fund to cover operating expenses or follow-on investments are these considered to be recycled under the LPA and how do these amounts increase the base for the preferred return calculation? Are preferred return provisions applied in the same way to amounts drawn over and above total commitment where allowed under the LPA? The LPA will clearly detail the funds’ recycling provisions however the impact on distributions and the preferred return is not always explicit.

- Systems – it is important that GPs have a proper technology strategy which is aligned to the calculation of the waterfall. There is a risk with complex calculations that either the manager, or in the case of an outsourced arrangement, the administrator, could make errors which ultimately affect investor returns. Langham Hall uses computable data to mitigate this risk, and allow us to handle complex waterfall calculations throughout the fund lifecycle.

If you are a first time GP wanting to understand the practical implications of an existing or proposed carry model, Langham Hall has a wealth of experience working with our clients and their service providers to define and interpret complex carry provisions and build quantitative models to support decision making.